Every second, thousands of people around the world open a can of Red Bull, Monster, Pepsi, or Coca-Cola. Few realise there’s a meaningful chance the caffeine inside originated from a factory in Tarapur, Maharashtra.

Long before that drink reached a supermarket shelf, someone at one of these global beverage giants placed a procurement order for caffeine. That order almost certainly went to one of just three suppliers: manufacturers in China, which control roughly 70% of global production; Germany, with about 10%; or a single Indian company based out of Tarapur.

That company supplies 15-20% of the world’s caffeine, meets nearly 80% of India’s domestic caffeine demand, and is the world’s only integrated non-Chinese manufacturer of caffeine.

That company is Aarti Pharmalabs Limited.

Aarti Pharmalabs: 1-Year Stock Price Movement

Source: http://www.tradingview.com

Yet, despite a dream run at the bourses after getting demerged from Aarti Industries, the stock has fallen roughly 22% over the last year.

What’s holding back the stock? Is the downtrend structural or simply a blip? Let’s dive in.

Understanding the business

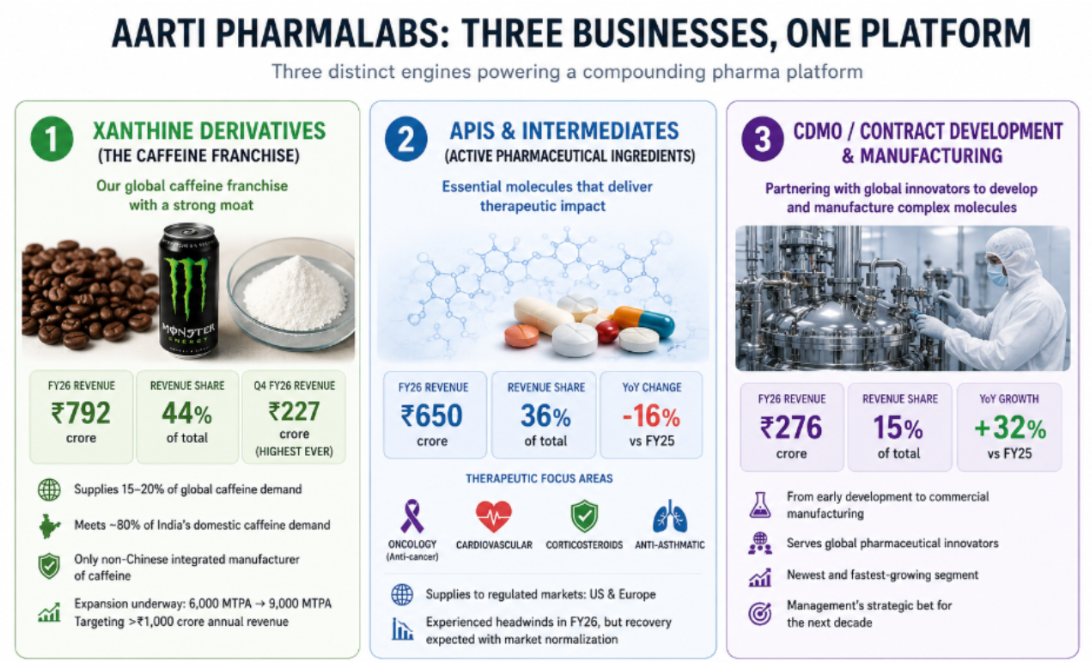

Aarti Pharmalabs is not just a caffeine business. It runs three businesses under one roof and has spent Rs 1,300-1,400 crore in cumulative capital expenditure over the last three years, building the infrastructure to grow all three simultaneously. FY26 alone saw Rs 400 crore deployed, with another Rs 400 crore budgeted for FY27. The stock has fallen roughly 22% over the last year. Whether that is the market being right about execution risk or missing an inflection point is exactly what this article aims to answer.

Source: Author illustration

The first is Xanthine Derivatives, the caffeine franchise. It reported Rs 792 crore in FY26, about 44% of total revenue, with its highest-ever quarterly number of Rs 227 crore in Q4 FY26.

The second is APIs and Intermediates. Aarti’s portfolio covers oncology, cardiovascular, corticosteroids, and anti-asthmatic APIs for the US and European markets. This segment contributed about 36% of FY26 revenue but had a difficult year, declining roughly 16% from FY25.

The third is Contract Development and Manufacturing (CDMO). Global pharmaceutical innovators pay Aarti to develop and manufacture complex drug molecules on their behalf, from clinical trial supplies through to commercial production. The newest and fastest-growing segment, up 32% year-on-year in FY26 to Rs 276 crore, and the one management is betting the company’s next decade on.

The caffeine moat nobody talks about

Think about what it takes to become a caffeine supplier.

You do not simply build a factory and win the business. Customer qualification typically takes two to three years before a single commercial kilogram is shipped. Buyers audit your facility, validate your manufacturing processes, and require internationally recognised certifications before approving you as a supplier. By the end of that process, you are no longer just a vendor, you’re deeply embedded in their supply chain, making switching both costly and disruptive.

That is why global caffeine manufacturing has only three serious players. Aarti’s 15-20% global market share is not just a statistic; it is an economic moat built over decades and reinforced through years of customer qualification.

The industry backdrop is also turning favourable. China has withdrawn its 13% export rebate on xanthine derivatives, removing a subsidy that had long suppressed global caffeine prices. At the same time, US tariffs are accelerating buyer diversification away from Chinese supply chains. As the world’s only integrated non-Chinese caffeine producer, Aarti stands to benefit from both trends

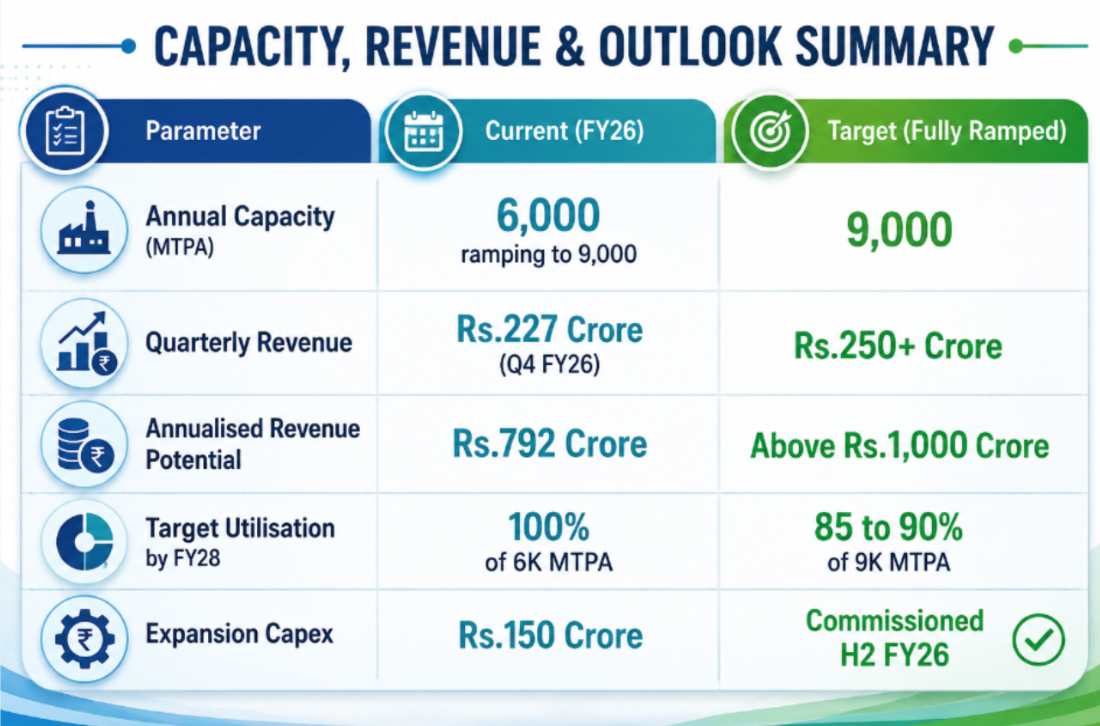

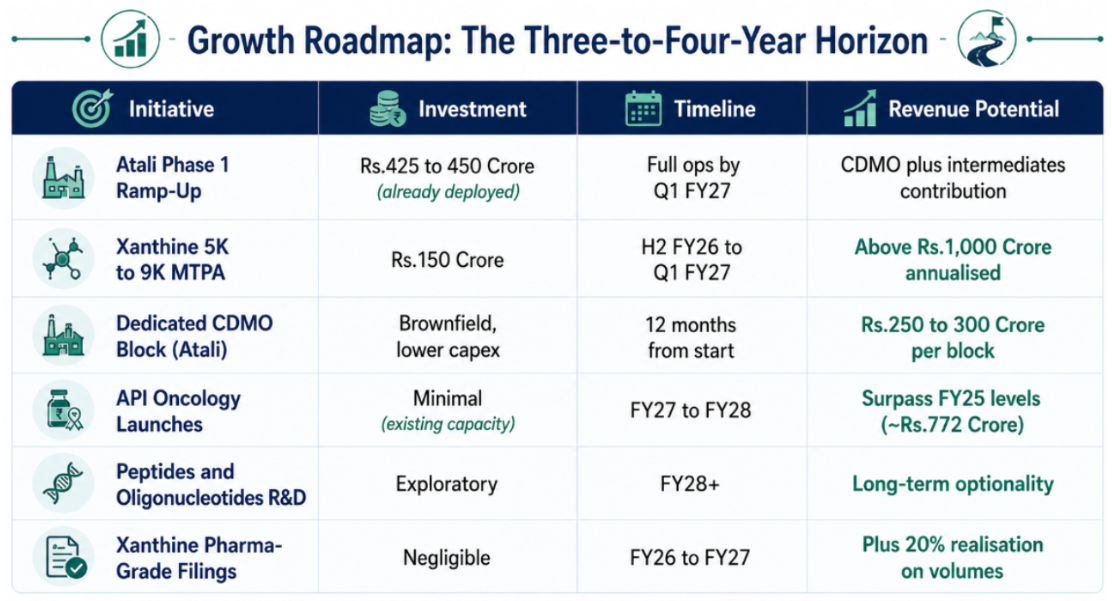

The expansion: From 5,000 MTPA to 9,000 MTPA

The economics of the expansion are straightforward. In Q4 FY26, Aarti generated Rs 227 crore of revenue from its 6,000 MTPA xanthine capacity. A Rs 150 crore investment will increase capacity by 50% to 9,000 MTPA, making management’s target of over Rs 1,000 crore in annual xanthine revenue a matter of execution rather than ambition.

At the same time, the company is securing US Drug Master Files and European CEP approvals for a second manufacturing site, enabling pharmaceutical-grade sales that command roughly 20% higher realisations than beverage-grade caffeine.

Source: Company filings, Q4 FY26 Earnings Call

The CDMO play and why Atali changes everything

CDMO is the smallest of Aarti’s three businesses today, but it carries the highest margin potential and some of the strongest customer stickiness.

Once a pharmaceutical innovator selects a CDMO partner for a commercial-stage molecule, switching suppliers requires regulatory re-filings, fresh validation, and years of work. That creates long-duration relationships and allows established CDMOs to command premium pricing.

Aarti has deliberately focused on late-stage and commercial molecules rather than early-stage development. As of FY26, 35 of its 54 active CDMO projects had already reached the commercial stage, while only 19 remained in development, resulting in a more predictable and lower-risk project mix.

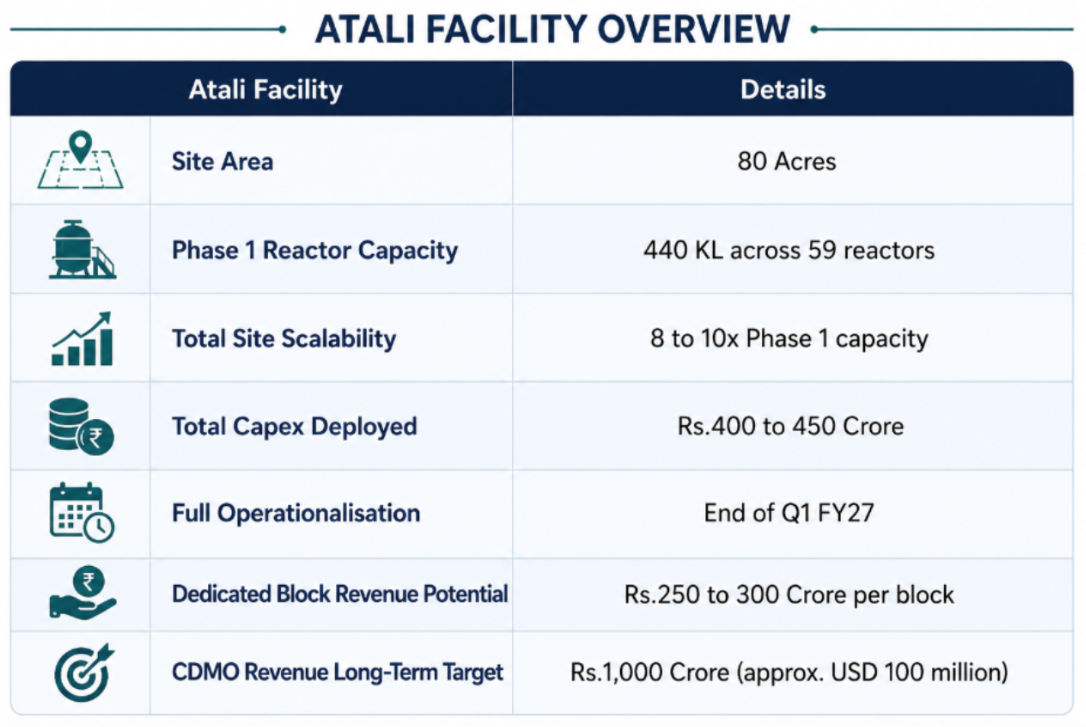

The Atali facility: Built for scale

Commissioned in September 2025, Atali is Aarti’s seventh manufacturing facility and its largest long-term CDMO investment. Phase 1 added 440 KL of reactor capacity across 59 reactors with a capex of Rs 400-450 crore, while the 80-acre site has been designed to support an expansion several times larger over the coming years.

Although the initial ramp-up weighed on Q3 FY26 performance, customer qualifications and operational improvements were largely completed by Q4, with full operationalisation expected by the end of Q1 FY27.

The bigger opportunity lies ahead. Management plans to add dedicated manufacturing blocks for long-term commercial CDMO projects, with each block expected to generate Rs 250-300 crore of annual revenue. Adding one block every year as new projects mature provides a clear blueprint for scaling the business over time.

Source: Company disclosures, Q4 FY26 Earnings Call

Near-term, management has guided 40-50% CDMO revenue growth for FY27, driven by Atali Phase 1 coming fully online and pipeline molecules progressing, including a recently approved product for hot flashes and a Phase 3 molecule targeting LDL reduction. Long-term, the company has announced R&D investments in peptides and oligonucleotides, newer modalities where global manufacturing capacity is scarce. These will not contribute in the near term, but they position Aarti for the next generation of pharmaceutical manufacturing demand.

APIs and intermediates: The business looking for its floor

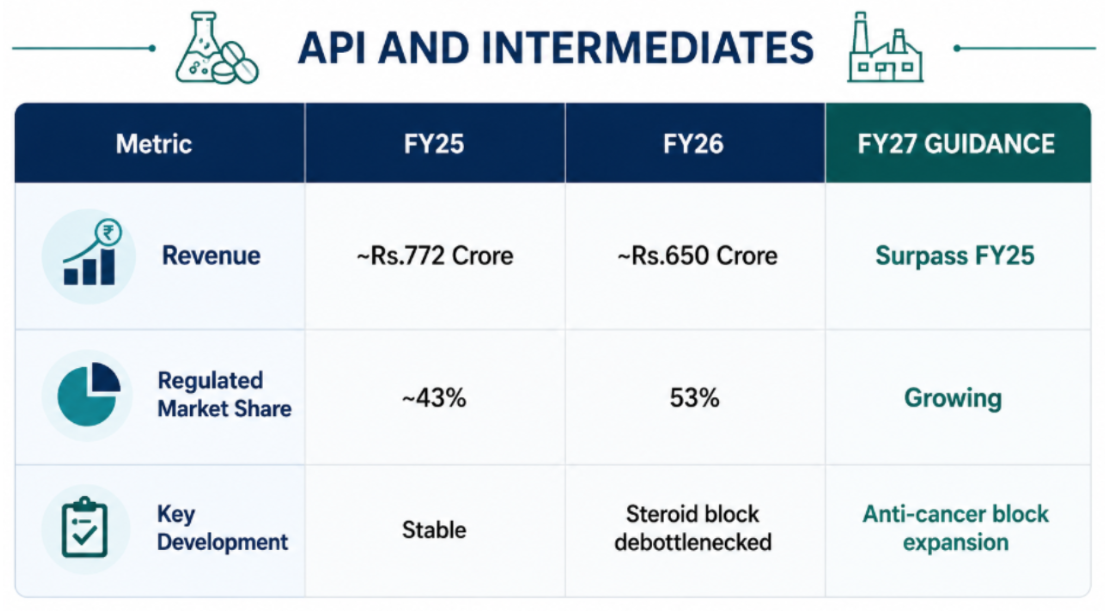

One of the core factors driving the stock sideways could be the poor performance in the API segment in FY26.

Revenue declined from approximately Rs 772 crore in FY25 to around Rs 650 crore in FY26, a fall of roughly 16%. Inventory destocking at customers, pricing pressure from Chinese API manufacturers, and startup-related cost absorption all hit simultaneously. It was a triple-headwind year.

The portfolio is not structurally impaired, though. Aarti’s API business is concentrated in high-potency categories: oncology, corticosteroids, and anti-asthmatic molecules. These are complex, USFDA-approved APIs with defensible margins, not commodity generics competing on price. In Q4 FY26, 53% of API revenue came from regulated markets. A steroid block debottlenecking at Tarapur Unit 4 increased steroid capacity by one-third in Q1 FY27, and an anti-cancer block expansion is planned through the year.

Management has guided that API revenue will surpass the FY25 level, driven by new oncology product launches. That is a recovery of over Rs 120 crore from the FY26 trough. Watch the quarterly cadence of new product launches as the primary signal.

Source: Company filings, Q4 FY26 Earnings Call

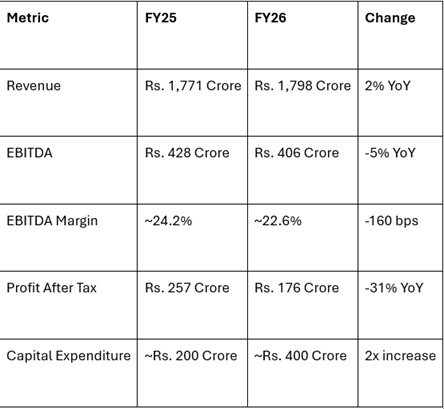

The numbers: A transition year in full view

FY26 was the year expansion costs ran ahead of expansion revenues. Rs 400 crore of capex went in. Revenue grew only 2%. EBITDA fell 5%. PAT fell 31%.

Summarised annual P&L statement

Source: Aarti Pharmalabs Q4 FY26 Earnings Call, May 26, 2026

Three things are worth noting. Strip out the Rs 33 crore forex loss, and the post-tax profit would have been closer to Rs 209 crore. The margin compression is entirely explained by new facility costs running ahead of revenues from those facilities, a pattern that corrects as Atali ramps up. And Rs 650 crore gross debt against Rs 406 crore annual EBITDA is manageable, not alarming, with management guiding net debt-to-equity toward 0.3-0.35x.

The most important sentence in the entire FY26 results, though, is this one from management: “From FY28 onwards, capex intensity will come down.”

Once you stop spending Rs 400 crore a year on greenfield construction and start harvesting revenue from assets already built, the P&L looks very different. That is the hinge on which the entire investment case turns.

Source: Company disclosures, Author Analysis

Management’s headline: 15-18% annual growth in both revenue and EBITDA over FY27 to FY30, with CDMO leading at 40-50% in FY27 specifically. If delivered, consolidated revenue approaches Rs 2,500-2,700 crore by FY29, and EBITDA potentially reaches Rs 650-750 crore, roughly 60-85% higher than FY26 levels.

Valuations: Priced for transition

At approximately Rs 6,400 crore market cap against FY26 EBITDA of Rs 406 crore, Aarti Pharmalabs trades at roughly 15-16x trailing EV/EBITDA (factoring in Rs 650 crore gross debt). Not expensive for a multi-segment growth story. Not cheap for a year where profitability declined, and the key facility was still finding its footing.

EV/EBITDA multiple historical chart

Source: http://www.screener.in

Disclaimer: What follows is a simple, illustrative if-then exercise to help you think about how the market might value a combined business. It is emphatically not a target price. The numbers here are placeholders built on management-stated segment figures and our estimates of the future.

The forward picture is more compelling. If the 15-18% EBITDA growth guidance holds through FY28, FY28E EBITDA would land in the range of Rs 530-560 crore. That implies approximately 13-14x forward EV/EBITDA for a business with a global caffeine oligopoly position, 54 active CDMO projects, and an 80-acre platform built for another Rs 1,000+ crore of revenue over time.

The re-rating trigger is not complicated: show sustained CDMO delivery. One or two strong CDMO quarters from Atali and the earnings trajectory inflects visibly upward, giving the market something concrete to price in rather than a promise to evaluate.

Risks worth noting

Atali execution is the most immediate concern. Phase 1 already experienced startup delays that hit Q3 FY26 hard. The market will watch Q2 and Q3 FY27 CDMO numbers closely.

CDMO customer concentration matters. With 21 customers across 54 projects, a single project timing shift can cause quarterly lumpiness. The business is not yet large enough to absorb individual programme delays without a visible earnings impact.

China remains a wildcard in Xanthine. The customer qualification moat is real, but if Chinese manufacturers aggressively expand capacity or any export rebate reversal occurs, pricing could come under pressure that Aarti cannot fully offset.

The API recovery is not guaranteed. FY26’s 16% revenue decline needs to reverse on the back of new oncology product launches. If those launches slip by a quarter or two, the recovery timeline extends.

Finally, Tarapur Unit 4 received a USFDA inspection in March 2026 with one observation in Form 483. Corrective measures are being submitted. Any escalation would directly hit the regulated-market API business.

Conclusion: Three engines, one key question

Aarti Pharmalabs has assembled an unusual combination: the world’s only non-Chinese integrated caffeine manufacturer, a CDMO business growing 32% with 35 commercial-stage projects, and a recovering API franchise in oncology and corticosteroids.

Rs 1,300-1,400 crore has been spent building this platform. From FY28, capex intensity drops while revenues from deployed assets accelerate. This transition from spending to harvesting is the single most important variable in the investment case.

The platform is built. The question now is whether the machines inside it run.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

Disclaimer: We do not own any of the content, ideas, images, or text presented here. All rights belong to their respective owners. For more information and to view the original source, please visit the following link: